With mixed results in 2014 in mining and metals, the opportunities for those in a position to take them has become significant. There is some very interesting information in the article I’m posting today. domain name generator . The results for the first half of 2014 really are a mixed bag but with joint ventures soaring and opportunities opening up due to the previous period of uncertainty, now is the time the next generation of mining heavyweights will emerge!

M&A and capital raising activity remained subdued over 1H 2014. This was largely the consequence of a continuing commitment to capital discipline and a lack of urgency over investment, given the relative lack of competition for assets.

Improving signals of economic growth in the US and the apparent subsidence of a looming emerging markets crisis have lowered broader market volatility. However, they failed to offset ongoing concerns surrounding growth in China and further near-term commodity price volatility.

As a result, the mining and metals industry lags a broader confidence revival in equity markets. Price weakness continues to place stress on certain sectors of the industry, despite management efforts to strengthen balance sheets and improve margins and returns.

For those brave enough to invest against the cycle, there would appear to be good buy-side opportunities, albeit driven by distress and opportunism, rather than out-and-out growth-seeking. The prospect of large-scale M&A remains unlikely for the industry’s majors.

But as we look ahead to the remainder of 2014, some factors suggest that momentum is building, including:

Some standout deals and hostile bids over the first half

A strong deal pipeline

Substantial capital waiting to be deployed by mining-focused funds

The recent and relatively rapid rise in the share prices of major mining and metals companies, on the back of improving base metals and gold prices, may prove to be a catalyst.

Deal activity falls, but sector outlook remains positive

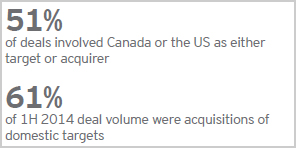

Mining and metals deal values in 1H 2014 are down 69% year-on-year, to $16.7b, from $53.8b, with deal volumes down 34% over the same period. So far this year, we have only seen 4 megadeals (>$1b), compared with 11 in the same period in 2013. Furthermore, 87% of first-half deals were valued at less than $50m, but comprised less than 8% of total deal value.

Divestments feed the pipeline

Who’s buying?

Major diversifieds continue to consider divestments as a way of reducing debt, maximizing return on capital and driving value across the portfolio.

However, with balance sheets largely stronger on the back of capital management, the urgency to divest has diminished and management can afford to focus on achieving an optimal exit for non-core assets.

What are they buying?

Depressed steel market drives activity

Overcapacity and lack of clarity around global demand growth continue to pose a challenging environment for steel, metallurgical coal and iron ore, which could lead to increased deal activity in these commodities.

As weaker steel producers struggle to stay afloat, stronger operators are likely to take advantage of their distress, buying up assets and using scale to

focus productivity on higher-margin capacity. More steel makers may consider divestment or possibly acquisition of downstream assets to reduce their exposure to the steel outlook.

Joint ventures to mitigate risks

We may see more joint ventures and mergers also in an effort to consolidate positions, achieve synergies and weather the continuing market uncertainty.

Many trading houses are actively selling their stakes in underperforming assets while still pursuing new joint ventures and alternative investment options in the mining space.

Outlook

Where are they buying?

We expect deal making to pick up from current levels, but with a continued focus on low risk transacting for the rest of 2014. The industry is waiting for some commodity price stability before taking any adventurous steps, so the next half year may prove to be a waiting game.

The emergence of competitive bids and execution of deals in the now strong pipeline should drive momentum.

An overall decline in proceeds raised in 1H 2014, to $142b from $168b, masks an ongoing divergence of fortunes within the mining and metals industry. As discussed in our Business risks facing mining and metals 2014-15.

and-metals) report, the “wealth gap” between producers and explorers appears to be widening.

The happy coincidence of thirst for yield among bond market investors and competition between banks for scarce major deal opportunities, against a backdrop of near-zero real interest rates, has proven a boon for borrowers in recent years.

Many mining and metals companies have been able to reduce borrowing costs further this year, and, critically, secure refinancing deals, as robust liquidity and strong demand has led to large and sometimes oversubscribed syndicates, driving down pricing and terms.

Risk-seeking supports mid-tiers, while project finance is back on the table

Sub-investment-grade borrowers took an increased share (35%) of total bond proceeds in 1H 2014, compared with previous years..

Project finance is also once again flowing into the industry’s growth projects – albeit on a highly selective basis. The mining sector saw a tenfold increase in project finance deals compared with 1H 2013.

Mining equities trail the confidence revival

Despite a recent rebound in mining and metals share prices, the Euromoney Global Mining and Steel index still hovers close to its 2009 trough, while the Dow Jones Industrials all-share index continues to reach new highs. Junior mining IPOs remain all but non-existent.

Secondary equity fundraising continues to be muted, with 40% of issues by juniors raising as little as $500,000.

Alternative financing sources are now a staple component of industry finance and continued to play an important role in 1H 2014.

Outlook: favorable debt markets for those who can take advantage

A narrowing of the wealth gap is unlikely to occur in the near-term. A sustained and expectation-beating commodity price recovery would be needed for risk investors to return to the exploration sector.

Being best-placed and able to spot and react to capital markets and other funding opportunities will increasingly provide a competitive edge in the advent of change.

Thanks to and the original article can be found by clicking this image.

Brilliant ideas and information you have here. I agree that “The results for the first half of 2014 really are a mixed bag but with joint ventures soaring and opportunities opening up due to the previous period of uncertainty, now is the time the next generation of mining heavyweights will emerge!” Much appreciated, you can post more regarding this blog.